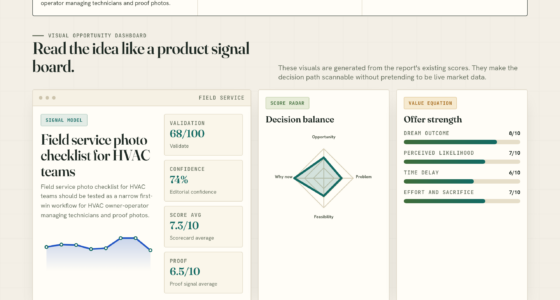

📊 Full opportunity report: The gigawatt gap. Why China is structurally positioned for AI power and the US is engineering around its grid. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

China’s centralized infrastructure and renewable energy buildout enable it to deploy AI data centers at gigawatt scale, substituting power throughput for chip performance. The US remains dominant in chips and models but faces constraints at the physical power delivery layer, creating a structural gap in AI infrastructure.

China has built a gigawatt-scale AI infrastructure network, leveraging its extensive renewable energy capacity and centralized planning, while the United States faces constraints at the physical power delivery layer, creating a structural gap in AI deployment.

Recent developments show China has added over 430 gigawatts of wind and solar capacity in 2025, surpassing US renewable additions by approximately eight times. This extensive buildout supports the deployment of large-scale AI data centers that operate at 1–2 gigawatts each, with some projects reaching 5 gigawatts.

Meanwhile, US AI infrastructure remains constrained by grid bottlenecks, permitting, and transmission issues, forcing American data centers to adopt workaround solutions such as off-grid gas turbines and nuclear contracts. The US leads in chip design, models, and AI applications, but its physical power delivery system limits deployment at the gigawatt scale.

Chinese chips, like Huawei’s Ascend 910C, perform at roughly 60% of NVIDIA’s H100 inference levels and lack native FP8/FP4 support. However, the Chinese strategy substitutes raw wattage for chip performance, enabled by the country’s large renewable capacity and extensive ultra-high-voltage transmission network, which spans over 40,000 kilometers.

The gigawatt gap.

Why China is structurally

positioned for AI power

and the US is engineering

around its grid.

power capacity end 2025

5-year average wait

45 projects · 340 GW capacity

vs. H100 · compensated by watts

interconnection queue

installed capacity

built by end-2024

on-site generation

DY 2024-25 → 2026-27

solar additions 2025

generation capacity

installed base

of capacity

add ratio

2025 alone

capacity end 2025

installed capacity

of capacity

Low watts

grid + transmission capacity

More watts

chip performance / FP precision

The US has perf-per-watt advantage. China has watts-without-bound advantage. These are asymmetric substitutes — not the same axis. When the perf-per-watt side is bounded by grid capacity and the watts-without-bound side is bounded by chip performance, the binding constraint differs.Thorsten Meyer · The Gigawatt Gap · Energy & Infrastructure 01

Implications of the Power Infrastructure Gap in AI Development

This structural difference in infrastructure fundamentally alters the competitive landscape of AI deployment. China’s ability to transmit vast amounts of renewable energy across its extensive grid allows it to deploy less powerful chips at scale, effectively closing the system-level performance gap faster than the US can improve chip efficiency alone. This challenges the assumption that chip performance alone determines AI capability at scale and raises questions about future technological and policy priorities.

For the US, the constraints at the power layer could limit the growth of frontier AI data centers, potentially capping AI development regardless of chip or model performance improvements. The outcome of this structural disparity could influence global AI leadership, economic competitiveness, and technological sovereignty in the coming years.

Tekpower TP-3005D-3 Digital Variable Triple Outputs Linear-Type DC Power Supply, 0-30 Volts @ 0-5 Amps

- Triple Output Voltage: 0-30V, 0-5A

- Dual Operation Modes: Constant Voltage & Current

- Automatic Cooling Fan: Thermo-sensor activated

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Structural Foundations of US and Chinese AI Infrastructure

The US has historically led in AI chip design, software, and applications, but its infrastructure is fragmented across federal, state, and local jurisdictions, complicating large-scale power deployment. Its reliance on off-grid solutions and regulatory arbitrage has allowed some workaround, but fundamental transmission bottlenecks persist.

China’s centralized planning through agencies like the NDRC and NEA enables coordinated expansion of renewable capacity and ultra-high-voltage transmission. The country’s focus on renewable buildout and extensive grid infrastructure allows it to transmit large amounts of power to AI data centers, even if individual chips are less performant than US equivalents. This structural advantage is rooted in the constitutional differences between the two countries’ governance models.

“The gigawatt-scale capacity requirements of frontier AI deployments are reshaping the infrastructure landscape, with China leveraging centralized planning and renewable energy to close the systemic power gap.”

— Thorsten Meyer

AI and IOT in Renewable Energy (Studies in Infrastructure and Control)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unresolved Questions About Future Infrastructure Dynamics

It remains unclear whether US efforts to improve chip efficiency and reform regulations will close the gigawatt gap or if China’s centralized infrastructure will maintain its advantage. The pace at which the US can address physical power constraints through policy or technological innovation is still uncertain, as is the long-term impact of China’s renewable expansion on global AI deployment.

maXpeedingrods Transmission Gear Shift Cable for Chevrolet Silverado 1500 2500 3500 1999-2007, GMC Sierra 1500 2500 3500 1999-2007 Automatic Transmission Shift Cable Kit 12477640

- Compatible Vehicles: Chevrolet Silverado and GMC Sierra 1999-2007

- Part Number: 12477640

- Easy Installation: Direct replacement, no modifications needed

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps in AI Infrastructure Competition

Over the next 24 months, key developments will include US policy reforms aimed at easing grid constraints, technological advances in chip efficiency, and China’s continued expansion of renewable and transmission infrastructure. Monitoring these efforts will clarify whether the US can overcome physical constraints or if China’s structural advantages will reshape the global AI landscape.

off-grid gas turbines for data centers

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Why does the US dominate AI hardware and models but lag in physical power infrastructure?

The US’s federal, state, and local governance creates fragmentation, complicating large-scale infrastructure projects. Its focus has been on chip design, software, and applications, while physical power delivery remains constrained by regulatory and transmission bottlenecks.

How does China’s renewable buildout support AI deployment?

China’s massive renewable capacity and extensive ultra-high-voltage transmission network enable it to transmit large amounts of power to AI data centers, allowing deployment at gigawatt scale despite less powerful individual chips.

Could US efficiency improvements close the gigawatt gap?

Potentially, yes. Advances in chip performance-per-watt and regulatory reforms could mitigate some constraints. However, whether these will be sufficient to match China’s infrastructure-based approach remains uncertain.

What are the risks if the gigawatt gap persists?

If the gap remains, US AI deployment could be limited by physical infrastructure constraints, potentially capping growth and affecting its leadership in AI innovation and applications.

Source: ThorstenMeyerAI.com