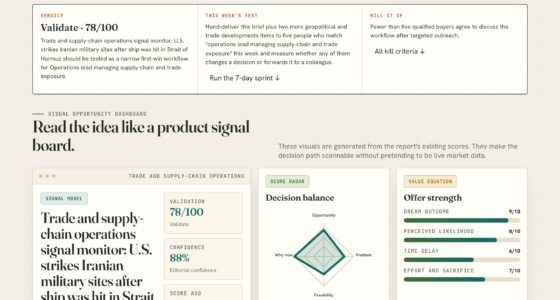

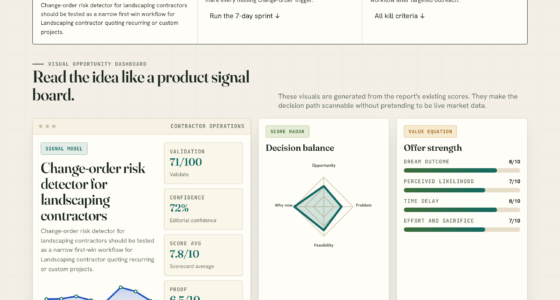

📊 Full opportunity report: The $60 Billion Bargain: Why Cursor Could Be a Steal for SpaceX on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

SpaceX announced the acquisition of Cursor for $60 billion, paid entirely in stock, with the deal valued as a bargain due to Cursor’s rapid revenue growth and strategic assets. This move aims to strengthen SpaceX’s AI and software infrastructure, with potential for high margins and competitive advantage.

SpaceX announced on June 16 that it has exercised an option to acquire Cursor, the AI coding tool startup, for $60 billion in all-stock. The deal, made just days after SpaceX’s historic IPO valuation exceeding $2 trillion, is a significant and strategic investment in AI and software infrastructure. The acquisition was completed without cash changing hands, with SpaceX issuing stock valued at a small percentage of its market cap, and the market responded positively, pushing SpaceX’s valuation higher.

Cursor, which has seen exponential revenue growth over recent months, is expected to reach a $6 billion annualized revenue by the end of 2026. Although the initial valuation of $60 billion appears high based on current revenue multiples, the multiple is rapidly decreasing as revenue accelerates. The deal was executed entirely in SpaceX stock, representing just 3.4% dilution at the IPO valuation, and caused SpaceX’s stock to rise approximately 16%, briefly making it the fourth-most-valuable company in the US.

Beyond its valuation, Cursor offers strategic value: it leads in profitable AI coding, with over a million paying users and 50,000 enterprise clients, including half of the Fortune 500. Its in-house-developed coding model, Composer, shipped in late 2025, already performs most of its work, and the company has rebuffed major competitors like OpenAI and Microsoft, gaining a competitive edge. The acquisition also enables SpaceX to internalize costs related to AI compute and API fees, which currently limit Cursor’s profitability, by integrating its AI stack with SpaceX’s own supercomputers and models through xAI.

The $60B bargain: why Cursor could be a steal

$60 billion for a code editor sounds like a bubble. Look past the headline and the price isn’t the scandal — it’s the discount. Here’s the case that SpaceX got Cursor cheap.

A melting multiple, paid in appreciating paper that cost almost nothing, for the profitable leader of the only AI category reliably making money — plus the missing app layer and an escape from the margin trap. If the growth holds and integration doesn’t break the product, $60B will read like a down payment. The risk isn’t overpaying for what Cursor is — it’s breaking what made it worth buying.

Strategic Impact of the Cursor Acquisition for SpaceX

This deal allows SpaceX to rapidly expand its AI capabilities within a profitable and fast-growing segment of generative AI, positioning it to dominate enterprise AI workflows. The acquisition reduces reliance on external AI providers, enabling higher margins through vertical integration. It also denies major competitors access to Cursor’s developer platform, strengthening SpaceX’s competitive position in AI tools and developer workflows. Given the market’s positive reaction and the deal’s structure, it exemplifies a strategic use of high valuation stock to acquire critical technology at a discount, potentially transforming SpaceX into a dominant player in AI-enabled software and automation.

AI coding software for developers

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Background and Growth Trajectory of Cursor

Cursor, developed by Anysphere, has experienced a remarkable revenue surge from $2 billion in February to an expected $6 billion by the end of 2026, making it the fastest-growing AI coding platform in history. Its rapid revenue ramp, combined with a profitable enterprise segment and a proven in-house coding model, has attracted attention from major industry players. Despite its growth, Cursor faced challenges with its suppliers, paying high API costs for frontier models, which limited margins. Its rejection of offers from OpenAI and Microsoft has kept it independent and positioned it as a strategic asset for a company like SpaceX, which owns its own AI infrastructure and models.

“This acquisition accelerates our AI and software capabilities, enabling us to better integrate AI across our aerospace and technology projects.”

— SpaceX spokesperson

enterprise AI coding tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Uncertainties Surrounding the Deal’s Long-Term Impact

While the deal’s structure and immediate market reaction are clear, it remains uncertain how effectively SpaceX will integrate Cursor’s technology and team into its broader operations. The long-term profitability of the combined entity depends on successful integration, continued revenue growth, and how well SpaceX can internalize AI costs. Additionally, the competitive landscape could shift if rivals acquire similar assets or develop alternative strategies.

programming code editor for professionals

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps for SpaceX and Cursor Integration

SpaceX is expected to begin integrating Cursor’s platform and team into its AI infrastructure in the coming months. The focus will be on leveraging Cursor’s proprietary models and developer tools to enhance SpaceX’s AI-driven projects, including satellite, rocket, and software development. Monitoring Cursor’s revenue growth and profitability post-acquisition will be key, alongside potential additional investments or strategic moves to solidify its AI leadership.

AI development platform

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Why did SpaceX pay for Cursor entirely in stock?

SpaceX used its own stock, which is highly valued, to acquire Cursor because it allowed the company to make a large strategic investment without immediate cash outlay, and the market’s positive reaction increased the value of this stock-based payment.

What makes Cursor a valuable asset for SpaceX?

Cursor offers a profitable, fast-growing AI coding platform with a large user base, enterprise clients, and its own proprietary models, making it a strategic foothold in enterprise AI workflows and developer tools.

How does this deal affect SpaceX’s overall valuation?

The market responded positively, boosting SpaceX’s valuation by about 16% on the announcement, pushing it close to $2.94 trillion and briefly past Microsoft and Amazon in market cap.

Could this acquisition impact competitors like OpenAI or Microsoft?

Yes, by acquiring Cursor and its developer platform, SpaceX effectively blocks competitors from gaining access to a key distribution channel, potentially shifting the competitive balance in enterprise AI tools.

What are the risks associated with this acquisition?

The main risks include challenges in integrating Cursor’s technology and team, maintaining rapid revenue growth, and the possibility that the strategic advantages do not materialize as expected.

Source: ThorstenMeyerAI.com